Originating from Japan, this distinguished Mazda 2 is renowned for its exceptional performance and reliability.

As a Sub-Compact Hatchback with a sleek 5-door hatchback body style, it radiates an air of refinement and style. Powered by a robust 1.5 I4 FWD engine paired with an efficient 6A gearbox, it offers an exhilarating driving experience. With 108hp and 139 Nm of torque at your disposal, acceleration from 0-100 kph takes a swift 10.5 seconds. You can enjoy cruising at a maximum speed of 185kph, while the impressive economy of 14.7 km/L ensures an efficient and cost-effective ride.

However, even with such an excellent collection of features, the cost of repairing the car in case of damage can pose a significant financial burden for owners. Thus, having the vehicle financially secured by Mazda 2 insurance becomes of paramount importance.

To learn more about Mazda 2 car insurance in the UAE, including its benefits and prices, keep reading this article.

Types of Mazda 2 Car Insurance Plans

When it comes to insuring your 2, there are two primary options to consider:

- Third-party insurance: Covers liabilities towards third-party injuries, death, and property damage, ensuring you’re protected if you’re held responsible for such incidents during an accident

- Comprehensive insurance: Provides all-inclusive coverage, including third-party liabilities, along with damage to your own Mazda 2 due to accidents, theft, fire, or vandalism. It also covers personal accident benefits for the driver.

Considering the value and significance of your 2, selecting the right insurance plan tailored to your needs is vital.

Average Mazda 2 Insurance Costs

Multiple insurance companies provide coverage for the Mazda 2, and prices can vary slightly based on the chosen insurer and plan.

On average, the annual premium typically starts from AED 1100 to AED 2500.

Factors Influencing Insurance Costs

The car insurance cost in the UAE depends on several factors, such as:

- Age of the Driver: The age of the driver plays a significant role in determining the insurance cost for a Mazda 2 in UAE. Younger drivers, particularly those under 25, are considered higher risk and therefore often face higher premiums. For example, a 22-year-old driver may pay more for their insurance than a 35-year-old driver.

- Driving Record: A clean driving record can significantly reduce the insurance cost for your Mazda 2. Drivers with a history of accidents or traffic violations are seen as high-risk, leading to increased premiums. For instance, a driver with two speeding tickets in the past year will likely pay more than a driver with no tickets.

- Vehicle Value: The Mazda 2, being a relatively affordable car, might attract lower insurance costs compared to luxury vehicles. However, a higher-end Mazda 2 model could result in higher premiums. For example, a Mazda 2 Sport with additional features would cost more to insure than a base model.

- Location: The area where you live and drive your Mazda 2 can impact your insurance costs. Areas with high traffic or crime rates may lead to higher premiums. For instance, living in downtown Dubai, with its high traffic density, might result in higher insurance costs than living in a quieter suburb.

- Coverage Type: The type and amount of coverage you choose for your Mazda 2 will directly influence the insurance cost. Comprehensive coverage, which includes damage from incidents other than collisions, will cost more than basic third-party liability coverage. For example, a policy covering theft, vandalism, and weather damage will cost more than a policy only covering damages to other vehicles in an accident you cause.

Tips to Reduce Your Car Insurance Premiums in the UAE

- Install anti-theft devices in Mazda 2

- Opt for a high deductible policy

- Maintain a clean driving record

- Limit the mileage of your Mazda 2

- Bundle insurance policies if possible

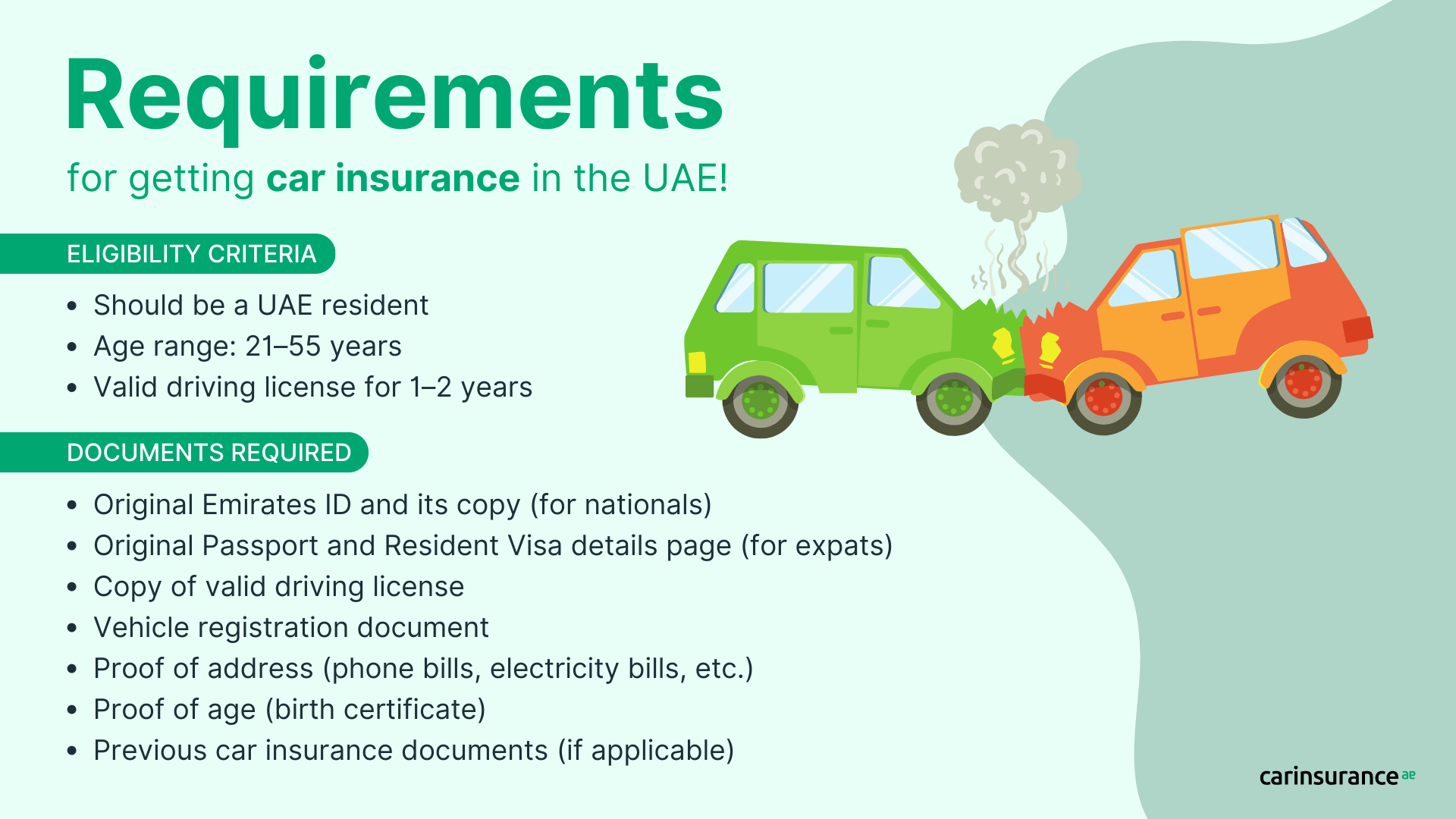

Eligibility Criteria and Documents Required

Obtaining Mazda 2 insurance is straightforward due to minimal eligibility criteria. Ensure you have the required documents for verification during the application process.

Best Mazda 2 Car Insurance Providers

Here are the best car insurance providers in the UAE that you can explore:

- AXA Redefining Insurance

- Union Insurance

- Oman Insurance Company

- Noor Takaful

- Dubai Insurance

How to Buy Mazda 2 Car Insurance in the UAE?

Ready to purchaseMazda 2 insurance in the UAE? CarInsurance.ae provides a seamless and hassle-free process.

We provide a convenient platform to compare various insurance plans from top providers all in one place. You can insure your dream car with just a few clicks.

Just follow these simple steps:

- Visit our Get Quotes page

- Select the Mazda, 2, and year of manufacturing of your car

- Select the city where you will be registering the insurance

- Enter the value of your car and specify any previous insurance claims

- Specify the duration of your UAE driving license

- Lastly, select the type of insurance coverage you prefer

And you’re done!

Upon completing these details, you will see a quote for your car. Begin the process now and protect your Mazda 2 with the coverage it deserves!

Also check:

FAQs

1. Are Mazda 2 cars expensive to insure?

The insurance cost for Mazda 2 in UAE can vary based on factors such as driver’s age, driving history, and coverage type, but it’s generally considered moderate compared to other models.

2. What to do in case of theft my Mazda 2 car?

In case of theft, immediately report to the local police and notify your insurance company with the police report.

3. Why should I buy comprehensive car insurance for my Mazda 2 car?

Comprehensive car insurance for your Mazda 2 is recommended as it covers all types of risks – accidents, theft, damages due to natural calamities, and third-party liability.